What Is a Systematic Withdrawal Plan (SWP) and How Does It Work?

Planning for income after you stop earning a regular salary is where investing becomes less about growth and more about stability. At that stage, the question quietly shifts from "How much can this grow?" to "How long can this last?" That is exactly where a Systematic Withdrawal Plan, or SWP, starts to make sense.

An SWP is essentially the reverse of systematic investing. Instead of putting money into a portfolio at regular intervals, you withdraw a fixed amount from your investments at a set frequency. This could be monthly, quarterly, or annually. It is commonly used in retirement, but it can also apply to anyone looking to generate steady income from an existing portfolio.

To understand how it works in practice, consider a simple scenario.

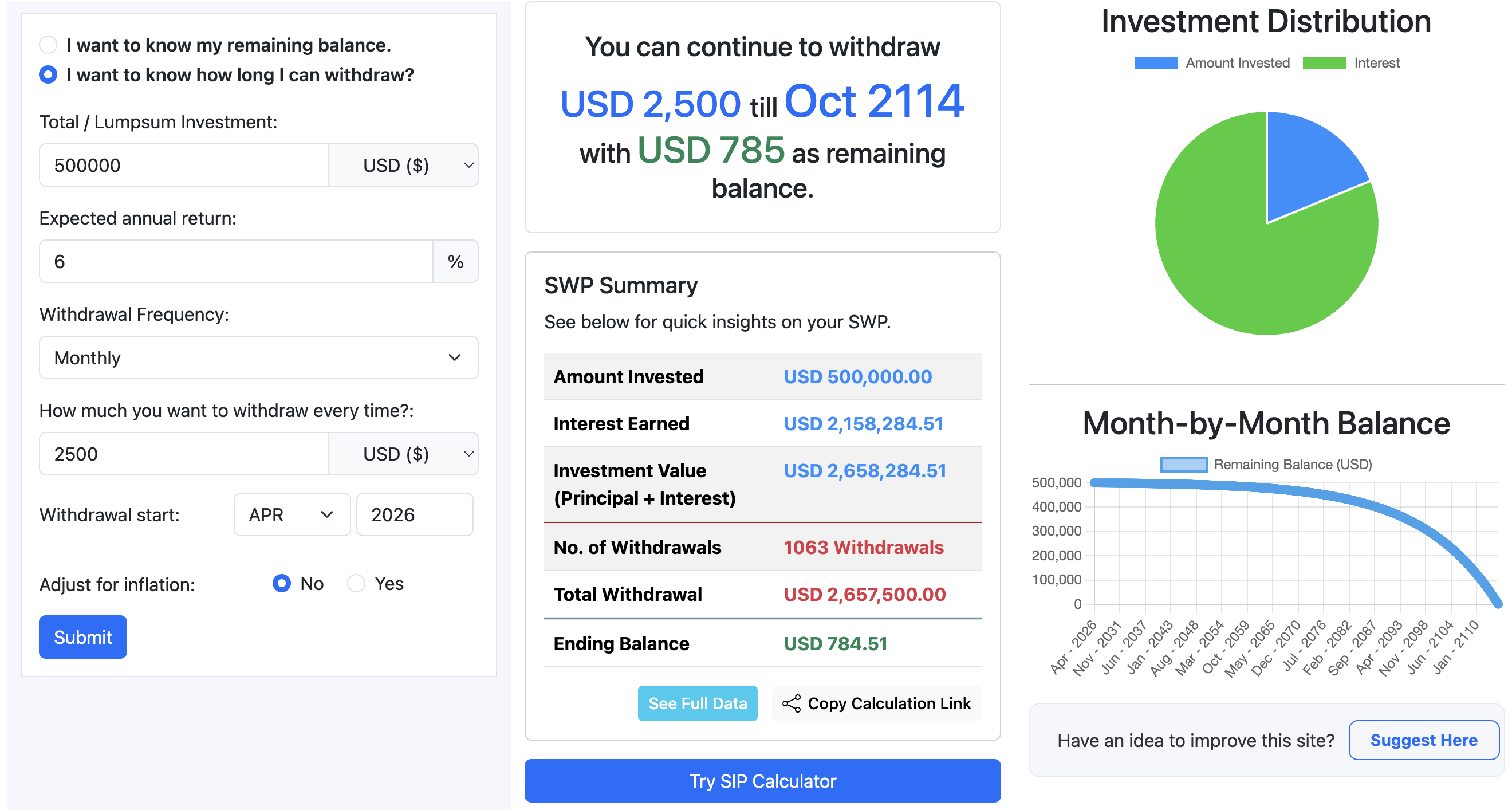

You have a portfolio worth 500,000 dollars. You decide to withdraw 2,500 dollars every month to cover living expenses. Your investments continue to stay in the market and generate an average return of 6 percent annually. Withdrawals are made monthly, while returns are assumed to compound over time.

At first glance, it feels sustainable. You are withdrawing 30,000 dollars per year, which is about 6 percent of the portfolio value. If your portfolio also grows at 6 percent, it might seem like the withdrawals and returns cancel each other out.

But real outcomes are rarely that symmetrical.

Over time, the portfolio gradually declines. Why? Because withdrawals are happening regularly, while returns are not evenly distributed. Markets fluctuate. Some years are strong, some are weak. Even if the long-term average is 6 percent, the timing of returns matters.

In this scenario, the portfolio would likely last around 25 to 28 years before being fully depleted, assuming returns remain close to the average and withdrawals stay constant. Over that period, you would have withdrawn roughly 750,000 to 840,000 dollars in total.

That sounds efficient on the surface. You started with 500,000 dollars and managed to withdraw significantly more over time. But the key detail is that the portfolio eventually runs out.

This is not a flaw in the strategy. It is simply the math of withdrawals interacting with compounding.

When you withdraw money, you are not just taking out cash. You are also reducing the base that generates future returns. Early withdrawals have a disproportionately large impact because they reduce the compounding potential of the remaining balance. This is often referred to as sequence-of-returns risk. If the market underperforms in the early years while withdrawals continue, the portfolio can shrink faster than expected.

Now consider a small variation.

If instead of withdrawing 2,500 dollars per month, you withdraw 2,000 dollars, the annual withdrawal drops to 24,000 dollars, or about 4.8 percent of the portfolio. That subtle difference can dramatically extend the life of the portfolio. In many cases, it may last well beyond 30 years, sometimes even preserving a residual balance.

On the other hand, if returns fall to 4 percent instead of 6 percent while maintaining the 2,500 dollar monthly withdrawal, the outcome shifts in the opposite direction. The portfolio may run out closer to the 20-year mark.

This is where SWPs become less about fixed formulas and more about flexible decision-making. The three variables that quietly control everything are:

- Withdrawal rate

- Investment returns

- Time horizon

Even small changes in any of these can significantly alter the outcome.

There is also the factor that tends to get underestimated: inflation.

If your expenses rise over time, a fixed withdrawal amount may not be enough. Increasing withdrawals to keep up with inflation puts additional pressure on the portfolio. A withdrawal rate that looked reasonable in year one can become aggressive over time if returns do not keep pace.

This is why many retirees do not stick to a rigid withdrawal plan. They adjust based on market conditions, portfolio performance, and personal needs. In strong market years, they may withdraw a bit more or reinvest less. In weaker years, they might cut back slightly to give the portfolio time to recover.

Coming back to the original scenario, withdrawing 2,500 dollars monthly from a 500,000 dollar portfolio with a 6 percent return sits in a borderline zone. It is not reckless, but it is not conservative either. It can work, especially if the time horizon is around 25 years. But it leaves little room for error if returns are lower than expected or if withdrawals increase.

A more sustainable approach often lies closer to a 3.5 to 4.5 percent annual withdrawal range, depending on market conditions and personal flexibility. Even then, it is not a guarantee. Markets do not follow fixed patterns, and long-term averages do not reflect the path taken to get there.

What makes SWP powerful is not just the structure, but the ability to adapt it. You are not locked into a fixed payout like some traditional income products. You retain control over your portfolio, your withdrawals, and your risk level.

Still, because outcomes are sensitive to multiple moving parts, rough estimates can only take you so far. This is where using a SWP calculator becomes genuinely useful. It allows you to test different scenarios, adjust return assumptions, tweak withdrawal amounts, and see how the timeline changes. Even a small adjustment can reveal whether your plan is comfortably sustainable or quietly drifting toward risk.

Most people underestimate how quickly things can change with just a one percent difference in returns or a slight increase in withdrawals. Running those variations through a calculator gives you clarity that static examples cannot.

In the end, an SWP is less about finding a perfect number and more about finding a balance. A balance between income today and security tomorrow. Between enjoying your money and ensuring it lasts.

If your withdrawals are aligned with realistic returns and you remain flexible when conditions shift, an SWP can provide a steady and controlled way to turn your investments into income. If not, it can quietly erode the very portfolio it depends on.