How to Use an SWP Calculator to Plan Your Retirement Income?

Retirement planning is often framed as a single question: how much is enough? But once you reach that number, a more practical concern takes over. How do you convert that pool of money into a steady income that supports your life without draining too quickly?

A Systematic Withdrawal Plan, or SWP, is one way to approach this. It allows you to withdraw a fixed amount at regular intervals while the remaining portfolio continues to stay invested and potentially grow. An SWP calculator helps you test whether your plan holds up over time or quietly falls apart.

Think of it less as a calculator and more as a reality check.

A Realistic Scenario

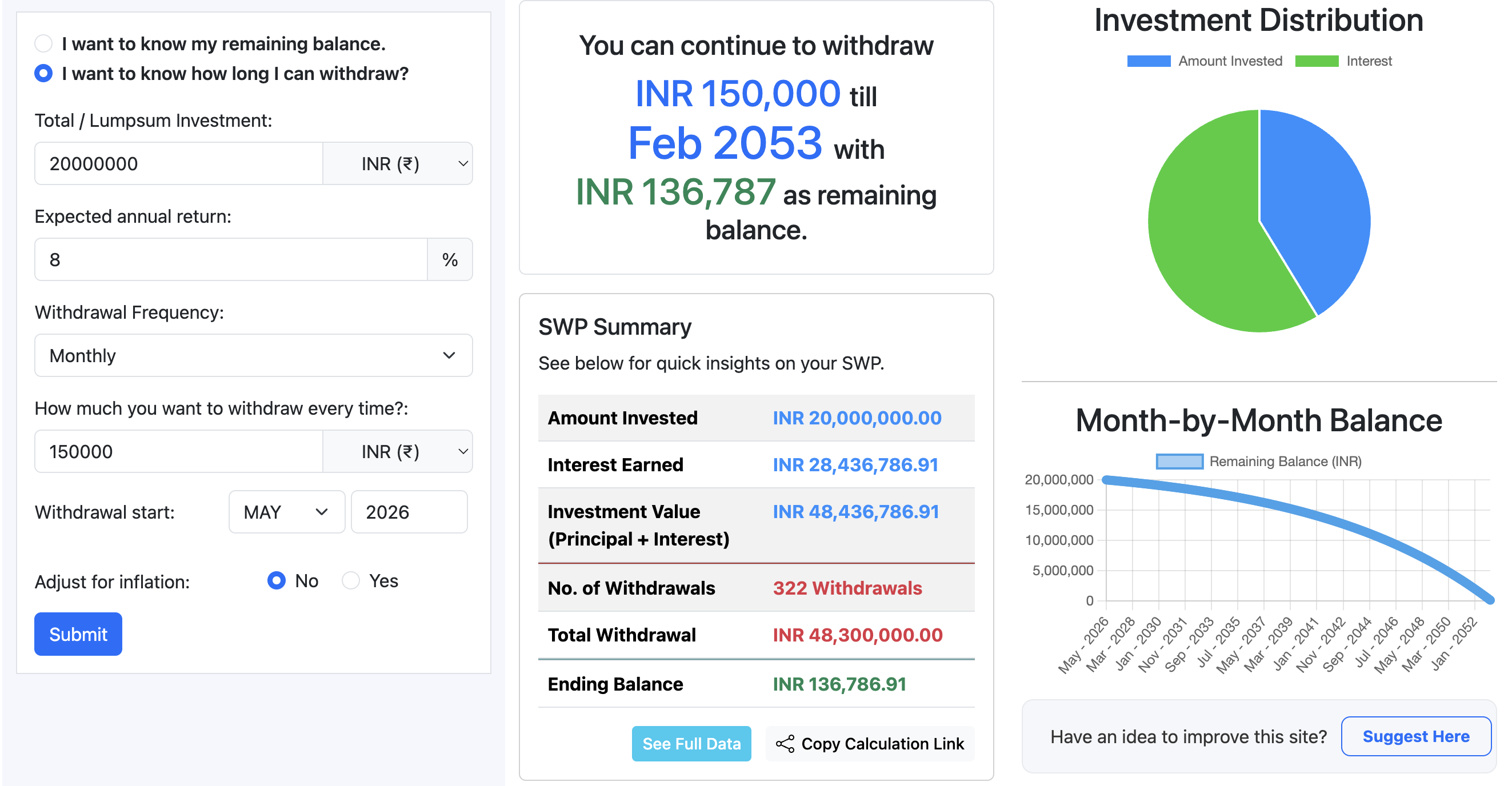

Consider someone retiring relatively early, at age 40, with a portfolio of 2 crore. They plan to withdraw 1.5 lakh every month and expect an average annual return of 8 percent.

At first glance, this seems structured and disciplined. The portfolio is sizeable, the withdrawal is consistent, and the return assumption is reasonable in a long-term sense.

But the real question is not whether this works for a few years. It is whether it can sustain decades of living expenses.

A monthly withdrawal of 1.5 lakh translates to 18 lakh annually. On a 2 crore portfolio, that is a withdrawal rate of about 9 percent per year.

That number deserves attention.

What the Outcome Looks Like

If you run this scenario through an SWP calculator, the trajectory becomes clear quite quickly.

Even with an 8 percent return, the portfolio struggles to keep up with the withdrawals. Over time, the gap between what you take out and what the portfolio earns begins to widen.

In practical terms, the portfolio would likely last somewhere in the range of 18 to 20 years (26 years maximum - if returns are always consistent - which is rare), depending on how returns are distributed over time. That means by your late 50s to mid 60s, the corpus could be significantly depleted or fully exhausted. ▶ Try This Scenario

For someone retiring at 40, that is a serious mismatch between lifespan and financial runway.

So while the plan appears workable in the short term, it is risky when viewed as a long-term retirement strategy.

Why This Happens

The core issue is the relationship between withdrawals and growth.

Your portfolio grows at an average rate of 8 percent annually. But you are withdrawing at a rate closer to 9 percent. That might not seem like a big difference, but over time it compounds in the wrong direction.

Each withdrawal reduces the base that generates future returns. As the portfolio shrinks, even consistent returns produce smaller absolute gains. Meanwhile, your withdrawals remain fixed.

Eventually, withdrawals dominate the equation.

This is why sustainability is not just about returns. It is about balance.

Where an SWP Calculator Becomes Useful

A good SWP calculator allows you to test exactly this balance.

If you have used one before, you have likely seen inputs such as total investment, expected return, withdrawal frequency, and start and end timelines. Some tools even let you toggle inflation adjustments or switch between viewing remaining balance and duration of withdrawals.

These are not just features. They are prompts to think deeper about your plan.

What happens if you reduce your monthly withdrawal slightly?

What if returns are lower in the first few years?

How long do you actually need your portfolio to last?

Instead of guessing, you can see how each decision shifts your financial path.

Small Changes, Big Impact

Take the same scenario and adjust just one variable.

If the monthly withdrawal drops from 1.5 lakh to 1 lakh, the annual withdrawal rate falls closer to 6 percent. That alone can extend the life of the portfolio significantly.

Or consider increasing the portfolio size before retirement. Even a moderate increase in the starting corpus can improve sustainability more than chasing higher returns.

Returns, after all, are uncertain. Your withdrawal rate is not.

Another important variation is inflation. In the current setup, withdrawals are fixed. But in reality, expenses tend to rise over time. If you increase withdrawals to keep up with inflation, the pressure on the portfolio becomes even greater.

What feels manageable today can quietly become unsustainable later.

The Reality Check Most People Skip

One of the biggest risks in early retirement planning is assuming that average returns will show up consistently.

Markets do not behave that way.

You could face a few weak years early in retirement. If that happens while you are withdrawing regularly, your portfolio may take a hit that is hard to recover from. This is known as sequence-of-returns risk, and it plays a critical role in SWP outcomes.

Two people with the same average return can end up with very different results depending on when those returns occur.

This is why a plan that looks fine on paper can fail in practice.

Is This Plan Sustainable?

Based on the numbers, withdrawing 1.5 lakh monthly from a 2 crore portfolio at an 8 percent expected return falls into the risky category for long-term retirement.

It may work for a decade or slightly longer, but it is unlikely to support a retirement that could span 30 or 40 years.

That does not mean early retirement is unrealistic. It means the structure needs adjustment.

You can:

Lower the withdrawal amount

Build a larger corpus before retiring

Combine withdrawals with some form of income

Adjust withdrawals dynamically based on market conditions

There is no single correct answer, but there are clearly unsustainable ones.

Using a Calculator to Think, Not Just Compute

An SWP calculator is not there to give you a single answer. It helps you explore boundaries.

You can test aggressive plans and see where they break. You can find a middle ground that balances lifestyle and longevity. You can prepare for uncertainty instead of assuming everything will go as expected.

It also forces you to confront trade-offs.

Higher withdrawals mean shorter portfolio life. Lower withdrawals mean adjusting your lifestyle. Higher returns help, but they cannot be guaranteed.

Seeing this visually often changes how people think about retirement planning.

Where This Leaves You

A 2 crore portfolio with a 1.5 lakh monthly withdrawal may feel comfortable at the start, especially if markets perform well early on. But over time, the math becomes harder to ignore.

The portfolio is being asked to do more than it realistically can, given the withdrawal rate.

Before locking into any plan, it is worth spending time with an SWP calculator and testing different scenarios. Not just once, but across multiple assumptions.

Because retirement income is not just about what works today. It is about what continues to work decades later.