SIP vs SWP: Which Is Right for You?

Most people don't start investing with a spreadsheet. They start with a question that's a lot more personal: am I trying to grow my money, or live off it?

That single distinction quietly decides whether a Systematic Investment Plan (SIP) or a Systematic Withdrawal Plan (SWP) makes more sense. Both work on the same underlying idea of disciplined, periodic transactions. But they operate in opposite directions, and the difference becomes very real when your portfolio starts funding your lifestyle.

Let's walk through how they actually behave, using a simple, realistic scenario.

A practical scenario: from building to withdrawing

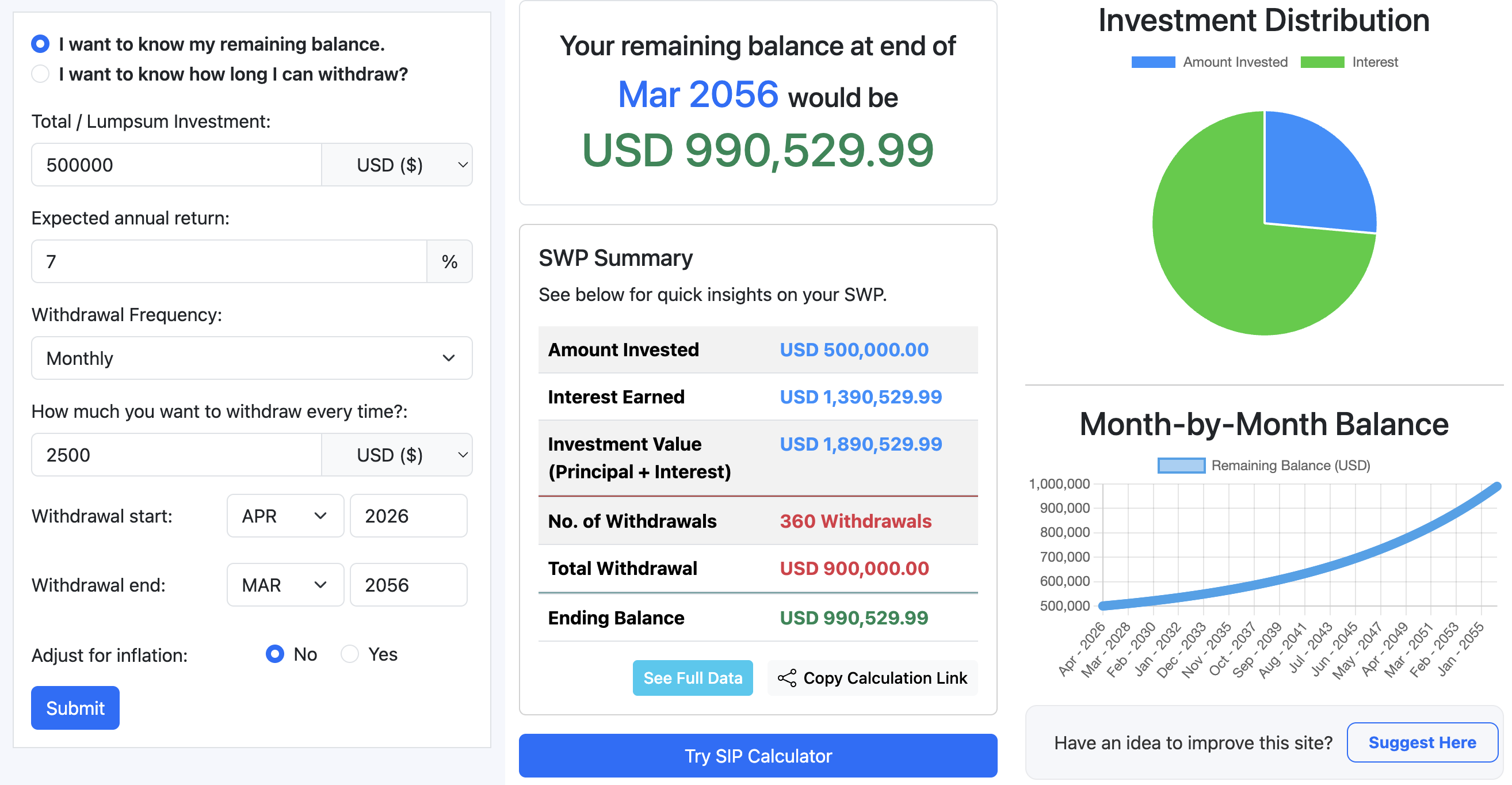

Consider someone who has built a portfolio of $500,000 over time using a SIP. Now they've reached a stage where regular income is needed, perhaps early retirement, a career break, or supplementing income.

They decide to switch to an SWP, withdrawing $2,500 per month. That's $30,000 per year, or about 6 percent of the starting portfolio annually. Assume the portfolio generates an average return of 7 percent per year.

At first glance, this looks balanced. The return slightly exceeds the withdrawal rate. But the interaction between returns and withdrawals is not linear, and that's where things get interesting.

What happens to the portfolio over time

If the portfolio consistently earns 7 percent annually and withdrawals remain fixed at $2,500 per month, the outcome is surprisingly stable.

After 10 years: ▶ Try This Scenario

- Total withdrawn: about $300,000

- Remaining portfolio: roughly $570,000

After 20 years: ▶ Try This Scenario

- Total withdrawn: about $600,000

- Remaining portfolio: around $710,000

After 30 years: ▶ Try This Scenario

- Total withdrawn: about $900,000

- Remaining portfolio: still in the range of $990,000

The portfolio doesn't just survive, it grows modestly despite continuous withdrawals.

That's the power of keeping withdrawals close to, but slightly below, long-term returns. Compounding continues to work in the background, even as money flows out.

In this scenario, the withdrawal appears sustainable over a long horizon.

Why this outcome occurs

The mechanics are straightforward but often misunderstood.

With a SIP, compounding works in one direction. You keep adding money, and returns build on a growing base. Time does most of the heavy lifting.

With an SWP, there's a constant tug-of-war:

- Returns push the portfolio upward

- Withdrawals pull it downward

If returns consistently exceed withdrawals, even by a small margin, the portfolio can sustain itself for decades. If withdrawals exceed returns, depletion becomes inevitable.

The key variable is not just the average return, but the gap between return and withdrawal rate.

When the balance shifts

Now adjust the same scenario slightly.

Instead of withdrawing $2,500 per month, increase it to $3,500 per month. That's $42,000 annually, or about 8.4 percent of the initial portfolio.

Everything else stays the same.

Now the picture changes.

After 10 years:

- Total withdrawn: about $420,000

- Remaining portfolio: roughly $395,000

After 20 years:

- Total withdrawn: about $840,000

- Remaining portfolio: around $185,000

By year 25 to 26, the portfolio is likely depleted.

This is no longer sustainable. It falls into the risky category.

The difference between $2,500 and $3,500 per month might not feel dramatic in day-to-day life, but over time, it determines whether your portfolio supports you indefinitely or runs out.

SIP vs SWP: the real distinction

A SIP is about accumulation. It suits phases where income is steady, expenses are covered, and the goal is long-term growth. Market volatility, while uncomfortable, often works in your favor through cost averaging.

An SWP is about distribution. It assumes your portfolio is now part of your income system. Stability matters more than aggressive growth, and the margin for error is smaller.

The shift from SIP to SWP is not just a strategy change. It's a mindset shift.

With SIP:

- You benefit from market dips

- Time smooths out mistakes

With SWP:

- Market dips can hurt early

- Timing and sequence of returns matter more than averages

The hidden risk: sequence of returns

Two portfolios can have the same average return over 20 years and still produce very different outcomes under an SWP.

If poor returns happen early, when withdrawals are already happening, the portfolio takes a hit that's hard to recover from. This is known as sequence-of-returns risk.

In the earlier example, the 7 percent return was assumed to be steady. Real markets don't behave that way.

A few bad years at the beginning could reduce the portfolio enough that even a reasonable withdrawal rate becomes borderline.

Inflation quietly changes everything

The scenario assumed a fixed withdrawal of $2,500 per month. In reality, expenses rarely stay constant.

If inflation averages 3 percent, maintaining the same lifestyle would require increasing withdrawals over time.

That means:

- Year 1: $2,500 per month

- Year 10: closer to $3,300 per month

- Year 20: over $4,500 per month

Now the effective withdrawal rate rises, even if the initial plan looked sustainable.

This is where many SWP strategies become borderline rather than clearly safe.

So which one is right for you?

It depends less on the product and more on your stage of life.

If you're still earning and building wealth, SIP is the natural choice. It aligns with long-term growth and reduces the need to time the market.

If you're drawing income from your investments, SWP becomes relevant. But it needs to be approached with more caution.

A sustainable SWP typically:

- Keeps withdrawals at or below expected long-term returns

- Accounts for inflation

- Allows flexibility in withdrawals during market downturns

A borderline SWP sits very close to the expected return rate and requires monitoring.

A risky SWP consistently withdraws more than the portfolio can reasonably generate.

Reality check: markets are not predictable

It's tempting to plan using clean, fixed numbers. But real portfolios experience volatility, changing returns, and unexpected expenses.

Even a well-planned SWP can run into trouble if:

- Returns are lower than expected for extended periods

- Withdrawals increase faster than planned

- Large withdrawals happen during market downturns

This doesn't mean SWPs don't work. It just means they require periodic adjustments.

Why running your own numbers matters

The examples above give a directional understanding, but small changes in inputs can lead to very different outcomes.

A slightly higher return assumption, a different withdrawal frequency, or a longer time horizon can shift the result from sustainable to risky, or the other way around.

That's why it's worth taking a few minutes to test your own scenario using a SWP calculator. It gives you a clearer sense of how long your portfolio might last, and how sensitive it is to changes.

A balanced way to think about it

SIP and SWP are not competing strategies. They are two phases of the same journey.

One builds the engine. The other runs it.

The challenge is knowing when to transition, and how much to draw without quietly undermining what you've built.

If your withdrawals are aligned with realistic returns and adjusted thoughtfully over time, an SWP can provide steady income without exhausting your portfolio.

If not, the same strategy can slowly erode your financial cushion without obvious warning.

The difference often comes down to a few percentage points, and the discipline to revisit assumptions as life and markets evolve.